Empowering Immediate Protection: Health Insurance Plan's That Doesn't Have Waiting Periods.

In the fast-paced world of today, health emergencies don't send advance invitations. Yet, traditional health insurance plans often impose waiting periods—those frustrating delays before you can claim benefits for certain conditions. These include the initial 30-day wait for non-accidental illnesses, 1-2 years for specific ailments like hernias or cataracts, and up to 4 years for pre-existing diseases (PEDs) such as diabetes or hypertension. For many customers, these periods feel like unnecessary barriers, especially when rising medical costs and unpredictable health issues demand instant coverage. A 2023 survey by the Insurance Regulatory and Development Authority of India (IRDAI) revealed that over 60% of policyholders cited waiting periods as a hinderance to buying or renewing health insurance.

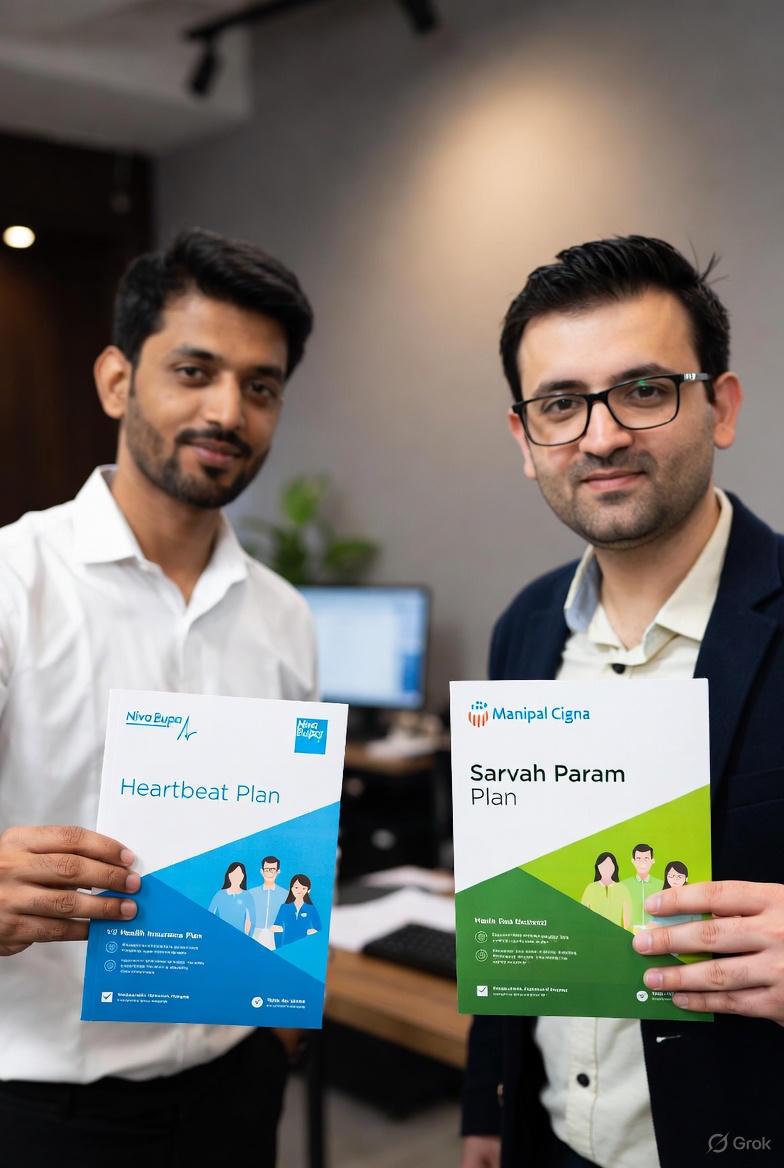

Customers today are vocal about their needs: they want plans that align with real-life urgencies, offering coverage from day one without the drag of exclusions. Fortunately, innovative insurers are listening. Enter plans like Niva Bupa's Heartbeat and ManipalCigna's Sarvah Param—tailored for those who refuse to let waiting periods stand between them and comprehensive protection. These options not only minimize delays but also prioritize accessibility, making health insurance a true safety net rather than a waiting game.

Niva Bupa Heartbeat: Swift Coverage for the Young and Active

Imagine signing up for health insurance and knowing that for most common procedures, you won't have to twiddle your thumbs for years. That's the promise of Niva Bupa's Heartbeat plan, a family-focused policy designed for immediate usability, particularly for those under 45 years old. Launched as part of Niva Bupa's commitment to hassle-free health security, Heartbeat eliminates the specific waiting period for insured individuals up to age 45, covering treatments for listed illnesses and procedures right away—think joint replacements, sinusitis, or piles, without the usual 24-month hold-up.

What sets Heartbeat apart is its blend of speed and breadth. The plan kicks off with a standard 30-day initial waiting period for non-accidental claims (waived for accidents, of course), ensuring you're protected almost from the get-go. For pre-existing conditions, coverage begins after 24-36 months, depending on the variant like Heartbeat Gold or Platinum, which is shorter than many competitors' 48-month timelines. Beyond waiting periods, Heartbeat shines with features like unlimited reinstatement of sum insured after claims, cashless treatment at over 10,000 network hospitals, and wellness rewards that can boost your coverage by up to 100% for healthy habits.

For a young professional like Priya, a 32-year-old marketing executive from Mumbai, Heartbeat was a game-changer. "I didn't want to risk a 2-year wait for something like a hernia surgery if it cropped up during my active lifestyle," she shares. With sum insured options from ₹5 lakh to ₹1 crore, premiums starting around ₹10,000 annually for a family of three, and add-ons for maternity (after a 9-month wait), Heartbeat appeals to millennials and Gen Z who prioritize agility over rigidity. It's not entirely waiting-free, but by axing specific delays for younger buyers, it bridges the gap between policy purchase and real-world readiness.

ManipalCigna Sarvah Param: The Ultimate Zero-Wait Revolution, Including Pre-Existing Peace

If Heartbeat trims the wait, ManipalCigna's Sarvah Param removes it entirely. Billed as a "zero waiting period health cover," this premium plan under the Sarvah series delivers on-the-spot protection for initial claims, specific diseases, and pre-existing conditions— a rare threesome in the Indian market. Through its default "Tatkal" benefit, coverage activates from day one, subject to underwriting approval, allowing claims for everything from a sudden flu to managing chronic hypertension without any postpone.

Pre-existing diseases, often the biggest hurdle for customers with ongoing health concerns, get the green light immediately—no 24-48 month limbo. This is particularly liberating for seniors or those with family histories of ailments; imagine a 55-year-old retiree like Rajesh from Bengaluru, who switched to Sarvah Param after his diabetes diagnosis. "Finally, a plan that doesn't punish me for my health history," he says. The optional "Pratiksha" benefit even lets you toggle on traditional waiting periods if preferred, but why would you? Specific procedures like varicose veins or benign tumors are covered sans delay, and the initial 30-day hurdle is history.

Sarvah Param isn't just about speed—it's a powerhouse of perks. Choose from sum insured up to ₹5 crore, with global coverage for emergencies, OPD benefits, and a "Surplus Benefit" that doubles your limit after the first claim. Annual premiums hover around ₹15,000-₹30,000 for a ₹1 crore cover, factoring in age and location. Backed by ManipalCigna's vast network of 8,500+ hospitals, it ensures seamless cashless claims. As per industry reviews, this plan has earned accolades for putting "Indian health needs first," resonating with over 40% of buyers seeking PED-friendly options.

Why Ditch the Delay? The Broader Impact on Customers

Waiting periods were born to curb adverse selection—insurers protecting against high-risk entries—but they've evolved into a customer pain point, leading to underinsurance or lapsed policies. Plans like Heartbeat and Sarvah Param flip the script, fostering trust and encouraging proactive health planning. By highlighting no-specific-wait for youth in Heartbeat and all-encompassing zero-wait in Sarvah Param, these products empower diverse demographics: active families, chronic condition managers, and everyone in between.

In a nation where healthcare spending hit ₹6.2 lakh crore in 2024, per NITI Aayog reports, immediate-access insurance isn't a luxury—it's essential. For personalized guidance tailored to your unique needs, reach out to your trusted insurance advisor, Felix A, who can help navigate these options and secure the right coverage without delay. Remember, the best policy is one that meets you where you are, not where it wants you to be in two years. Your health can't wait—neither should your coverage.

Consult Now for Zero-Waiting-Period Health Insurance!

by Felix A

by Felix A